A quick story IB Economics students recognise

The night before a mock exam, a GDP line on a graph can feel like a heart monitor: up, down, flat, panic. In IB Economics, that single line is more than a trend. It’s the story of jobs, wages, public services, and sometimes the environment paying the bill. If you can explain economic growth clearly, you unlock a big chunk of Macroeconomics: definitions, data response, AD/AS diagrams, and evaluation.

This guide breaks down what economic growth is, how to measure it, what causes it, and how to write about it like an examiner is reading.

Economic growth: the IB Economics definition

In IB Economics, economic growth means an increase in real output over time, usually measured by real GDP. “Real” matters because it removes inflation, letting you compare actual production across years.

For syllabus-aligned wording and diagrams, use Economic growth notes (3.3.1) and keep the core definition ready for Paper 1.

Exam checklist: what to know in IB Economics

-

Define economic growth using real GDP

-

Distinguish nominal vs real values

-

Calculate or interpret growth rates

-

Use GDP per capita for living standards

-

Explain demand-side (AD) vs supply-side (LRAS) growth

-

Evaluate benefits vs costs (inequality, inflation, environment)

-

Link growth to the business cycle

If you want quick recall cards for definitions and formulas, pair this with Macroeconomics flashcards.

Measuring economic growth (the numbers examiners love)

Real GDP

-

Nominal GDP measures output using current prices.

-

Real GDP adjusts for inflation.

A common method:

Real GDP = (Nominal GDP ÷ GDP deflator) × 100

In IB Economics data-response questions, real GDP is the safer indicator for “did the economy actually produce more?” rather than “did prices rise?”

GDP per capita

GDP per capita helps you discuss average living standards:

GDP per capita = Real GDP ÷ Population

It’s especially useful when comparing countries of different sizes. For a deeper explanation you can quote in evaluation, see Real GDP/GNI per person notes (3.1.6).

Growth rate

Economic growth is often expressed as a percentage change:

Growth rate = [(Real GDP this year − Real GDP last year) ÷ Real GDP last year] × 100

A simple Paper 2 habit: always state whether you’re describing short-run fluctuations or long-run trends.

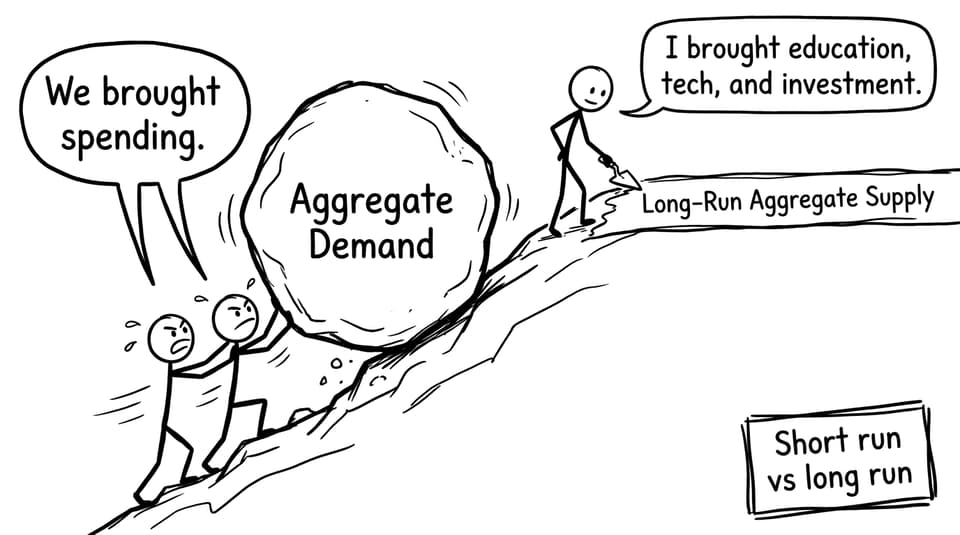

What causes economic growth in IB Economics?

In IB Economics, you’ll usually frame causes using the AD/AS model.

Demand-side growth (short run)

Short-term growth happens when aggregate demand rises (AD shifts right). Common drivers:

-

Higher consumption (C)

-

Higher investment (I)

-

Higher government spending (G)

-

Higher net exports (X−M)

This is the type of growth linked to booms in the business cycle and can bring inflation if the economy is near full employment.

Supply-side growth (long run)

Long-term growth is about increasing productive capacity (LRAS shifts right). It’s driven by:

-

Education and training (human capital)

-

Technology and innovation

-

Capital investment

-

Better institutions and productivity

This is the growth you describe as “sustainable” in the economic sense: output rises without automatically triggering inflation.

To tighten your terminology, use the IB Economics glossary when you revise.

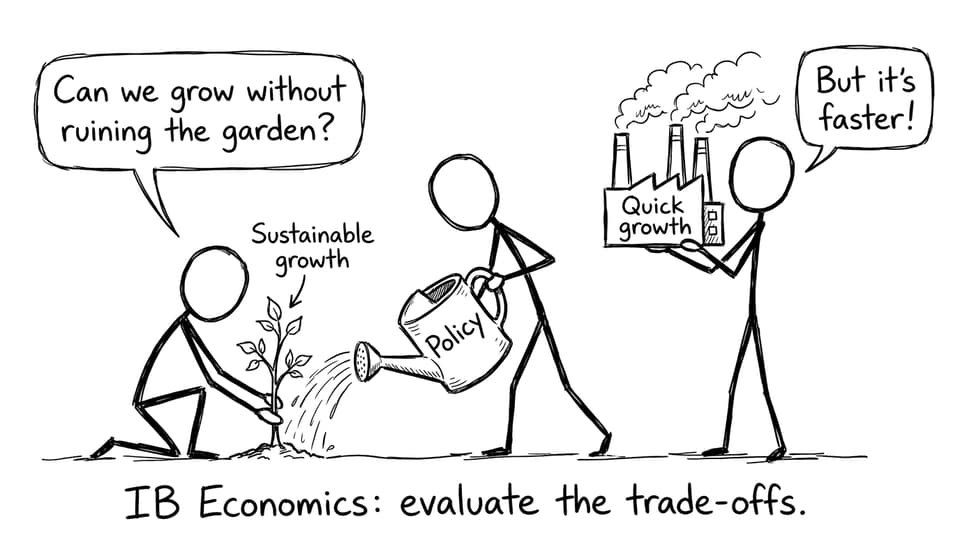

Benefits, costs, and the evaluation that earns marks

Economic growth can bring:

-

Higher incomes and employment

-

Higher tax revenue for public services

-

Improved material living standards

But IB Economics expects you to weigh trade-offs:

-

Inflationary pressure if AD rises too fast

-

Income inequality if gains are uneven

-

Environmental damage if growth relies on pollution-heavy output

The difference between an average answer and a top answer is often one sentence of balance: “However, the extent depends on spare capacity, the distribution of income, and whether growth is driven by productivity or pure spending.”

For more exam-structure support, see Top IB Economics HL mistakes and how to avoid them.

Sustainable economic growth (the “so what?” in IB Economics)

Sustainable growth means meeting current needs without harming future welfare. In IB Economics, it connects macro objectives to real policy choices: cleaner technology, renewable energy, and inclusive growth that doesn’t leave groups behind.

If you want to extend beyond the basic growth definition into policy strategies, explore Economic growth and development strategies (Topic 4.10).

Closing: turn economic growth into easy marks

Economic growth is one of those IB Economics topics that looks simple until you meet a messy data set or a “to what extent” essay. Keep it steady: define it with real GDP, measure it with growth rates and GDP per capita, explain it with AD/AS, then evaluate trade-offs like inflation, inequality, and sustainability.

When you’re ready to practise under exam conditions, RevisionDojo is built for it: Mock Exams, Predicted Papers, a topic-by-topic Questionbank, exam-ready Study Notes, active-recall Flashcards, AI Chat for instant clarification, a Coursework Library, and expert Tutors to push your evaluation to grade 7 level. Start with the RevisionDojo IB Economics hub and make economic growth one of your most reliable marks.