In IB Economics, markets often look neat on the page: buyers compare prices, sellers compete, and resources flow to their best use. Then real life walks in--and someone knows something you don’t.

That quiet gap is asymmetric information: one side of a transaction has better information than the other. In IB Economics, it matters because when information is uneven, prices stop being reliable “signals.” And when prices stop guiding decisions well, markets drift into market inefficiency.

The IB Economics checklist: how information gaps break markets

Use this quick checklist for essays and short responses in IB Economics:

-

Hidden information (before purchase) leads to adverse selection

-

Hidden actions (after purchase) leads to moral hazard

-

Mispricing becomes common (wrong price for quality/risk)

-

Trust falls, so quantity traded falls

-

Competition weakens because quality is harder to prove

If you want syllabus-aligned definitions, keep a tab open to the IB Economics glossary.

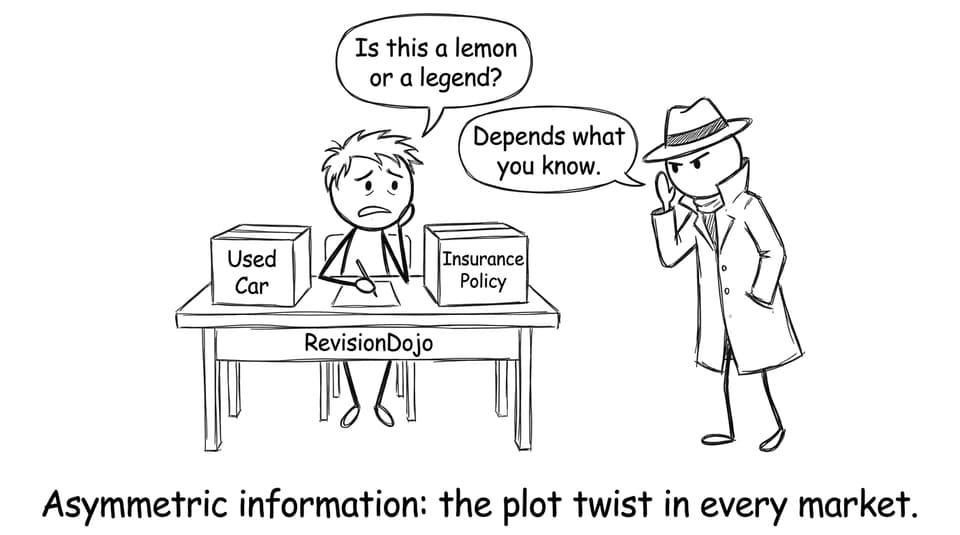

Adverse selection: the market loses the “good stuff”

In IB Economics, adverse selection happens before the transaction, when buyers can’t tell high quality from low quality. The classic example is the used car market: sellers know whether a car is excellent or a “lemon,” but buyers can’t verify.

So buyers protect themselves by offering only an average price. High-quality sellers then leave because the price is too low. The market becomes dominated by low quality. Trades that should have happened don’t happen--a clear inefficiency and misallocation of resources.

For targeted practice, RevisionDojo’s 2.10 Market Failure - Asymmetric Information Questionbank is built for exactly this kind of exam explanation in IB Economics.

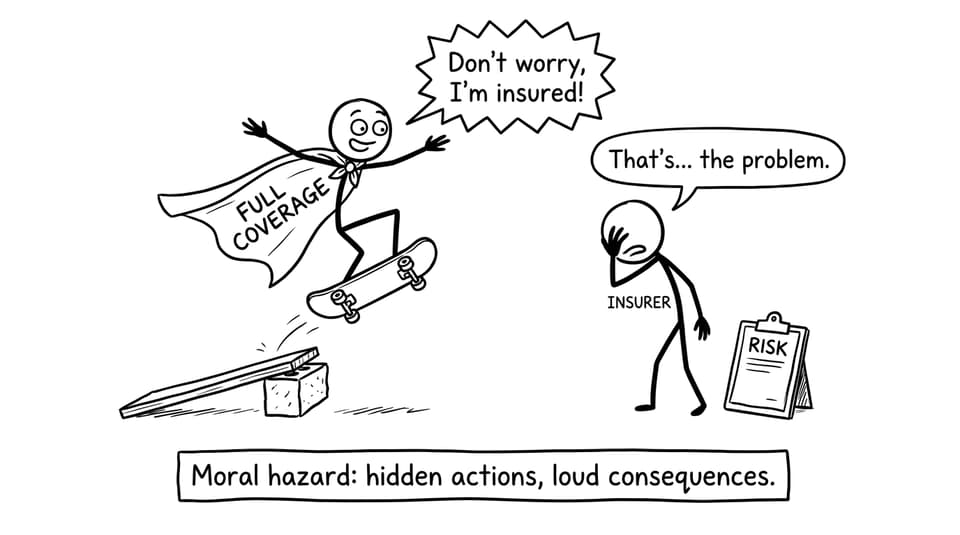

Moral hazard: incentives shift after the deal

Moral hazard is the “after” problem in IB Economics. One party can take actions that the other party can’t fully observe, and those hidden actions change behaviour.

Insurance is the cleanest example: with full coverage, a person might take fewer precautions because they won’t bear the full cost if something goes wrong. Risk rises, costs rise, and the market outcome moves away from efficiency.

Mispricing and missing trades: when the price signal fails

A lot of the inefficiency in IB Economics comes down to a simple idea: when buyers can’t observe quality or risk, the price mechanism can’t do its job.

-

If buyers underestimate quality, they demand a lower price and sellers may exit.

-

If sellers hide risk and buyers suspect it, demand can collapse.

Either way, the quantity traded falls even when trade could have improved welfare. That lost exchange is the part students often forget to mention--but examiners love it.

For broader context, see how this fits with other failures in How Market Failures Interact in Real Economies.

Fixing the gap: signalling, screening, and smart policy

Markets don’t just give up. In IB Economics, common solutions include:

-

Signalling (e.g., brand reputation, qualifications)

-

Screening (e.g., interviews, checks, trials)

-

Warranties and certifications

-

Government regulation and provision of information

A strong extension point is linking solutions to trust: institutions exist to make information credible. RevisionDojo explains this clearly in How Do Warranties and Signalling Help Solve Information Problems?.

If you’re revising the full syllabus section, use 2.10.1 Asymmetric information and the follow-up notes on 2.10.2 Responses to asymmetric information.

Conclusion: turn information into an exam advantage

Asymmetric information leads to market inefficiency in IB Economics because it distorts incentives and weakens the price signal: adverse selection removes high-quality options, moral hazard increases risky behaviour, and mistrust reduces trade.

To revise it quickly and properly, use RevisionDojo as your home base: the Study Notes clarify the theory, the Flashcards lock in definitions, the Questionbank builds exam timing, and AI Chat helps you test explanations. Add Mock Exams, Predicted Papers, and Grading tools when you want realistic feedback, and use the Tutors if you need a personalised push. In IB Economics, information is power--so revise like someone who has it.