This site uses cookie tracking technologies. Learn more in our Cookie Policy.

IB Economics: How Production Costs Shift Supply | RevisionDojo

Join 600k+ students breezing through the IBReady to breeze through the IB?

Production costs rarely make headlines. But in IB Economics, they quietly decide whether firms expand output, cut back, or freeze entirely.

Picture a small bakery the week before your mocks. The price of flour jumps, electricity costs spike, and staff ask for higher wages. Nothing about customer demand changed. Yet the owner still bakes fewer loaves. That moment is the syllabus in real life: changes in production costs affect supply decisions because they change what firms can profitably produce.

Cost shocks comic

The exam-ready idea (one-sentence definition)

In IB Economics, higher production costs reduce firms’ willingness and ability to supply at every price (supply shifts left), while lower costs increase it (supply shifts right).

Why production costs affect supply decisions in IB Economics

Profitability is the steering wheel

Firms don’t produce “because.” They produce because the gap between revenue and cost leaves a profit worth chasing.

When production costs rise, marginal cost tends to rise too. At each possible market price, fewer units remain profitable, so firms reduce output. In diagram terms, this is a leftward shift of supply.

When production costs fall, more units are profitable at every price. Firms can supply more, so supply shifts right.

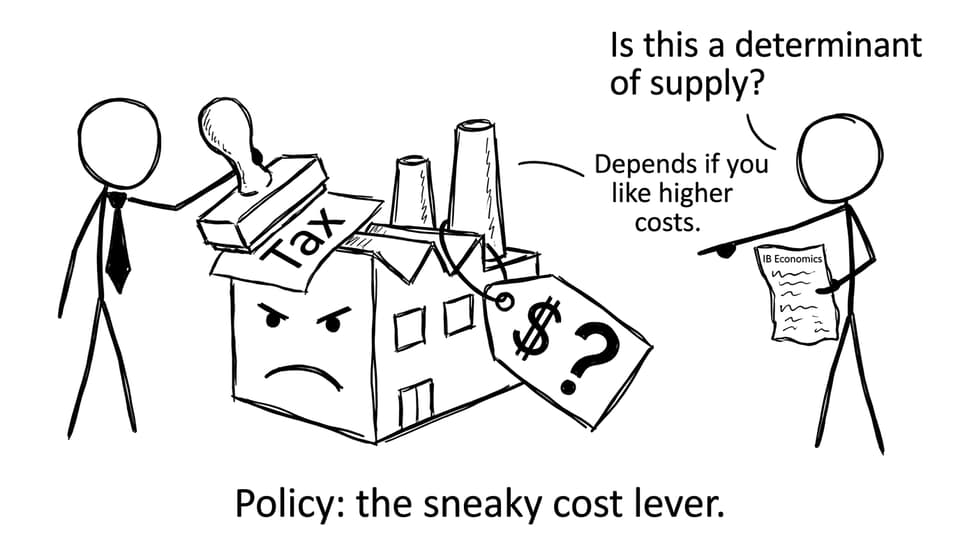

Many industries are basically “input conversion machines.” If a key input gets expensive, supply contracts.

Wheat up? Bakeries face higher unit costs.

Oil up? Airlines, delivery firms, and plastics producers feel it quickly.

Shipping disruptions? Even if demand is strong, supply can fall because each unit is harder and more expensive to produce.

That’s why cost shocks cause market outcomes that look like “sudden shortages,” even without any demand shift. If you want to link this to market outcomes, use Understanding Market Equilibrium in IB Economics.

Cost structure race comic

Technology lowers costs and expands supply

Technology is the calm, long-term force that makes supply feel easier. Better machinery, automation, inventory systems, and forecasting can reduce waste and labour time, lowering unit costs.

In IB Economics, your chain of reasoning should sound like this:

Technology improves --> unit costs fall --> firms are willing and able to supply more --> supply shifts right.

Supply decisions aren’t moral choices. They’re accounting choices. In IB Economics, changes in production costs matter because they reshape profitability, planning confidence, and competitive pressure, which shifts supply and moves markets to new equilibrium outcomes.

If you want to turn this into easy marks, build a simple routine on RevisionDojo: review the supply notes, drill flashcards, hit the Questionbank, then pressure-test your understanding with predicted papers and mock exams. That’s how “production costs affect supply decisions” stops being a paragraph you memorise and becomes a diagram-and-explanation you can deliver on demand.